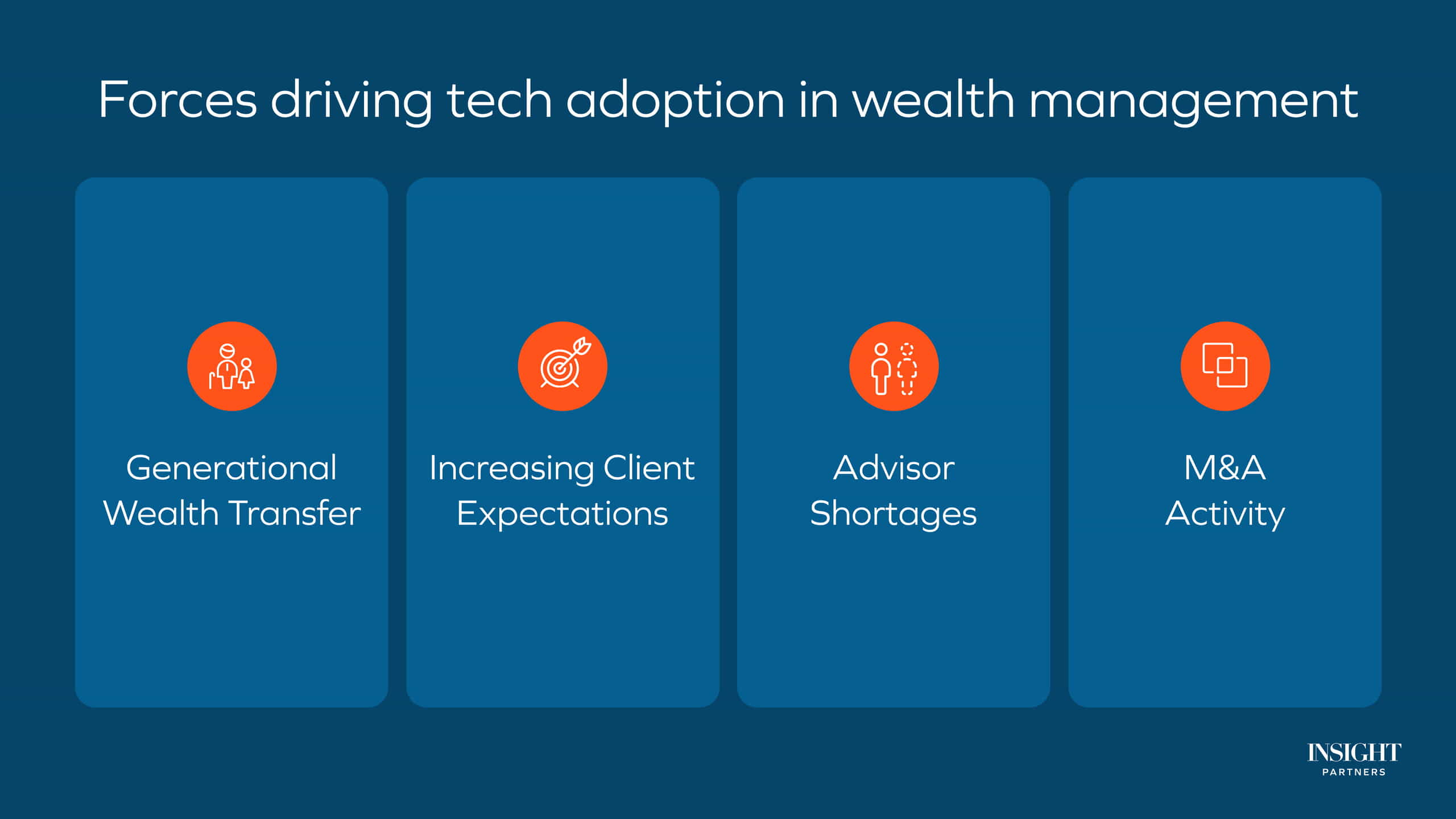

Wealth management is entering a period of change. A historic generational wealth transfer is underway, and client expectations are rising while the advisor workforce is shrinking. Registered investment advisors (RIAs) are under pressure to do more with less.

A new generation of WealthTech companies is emerging to solve these challenges. By automating workflows, unifying data, and augmenting advisor capabilities with AI, companies are reshaping how wealth firms serve clients.

The winning RIAs won’t just have great advisors — they’ll have great systems that enable great advisors.

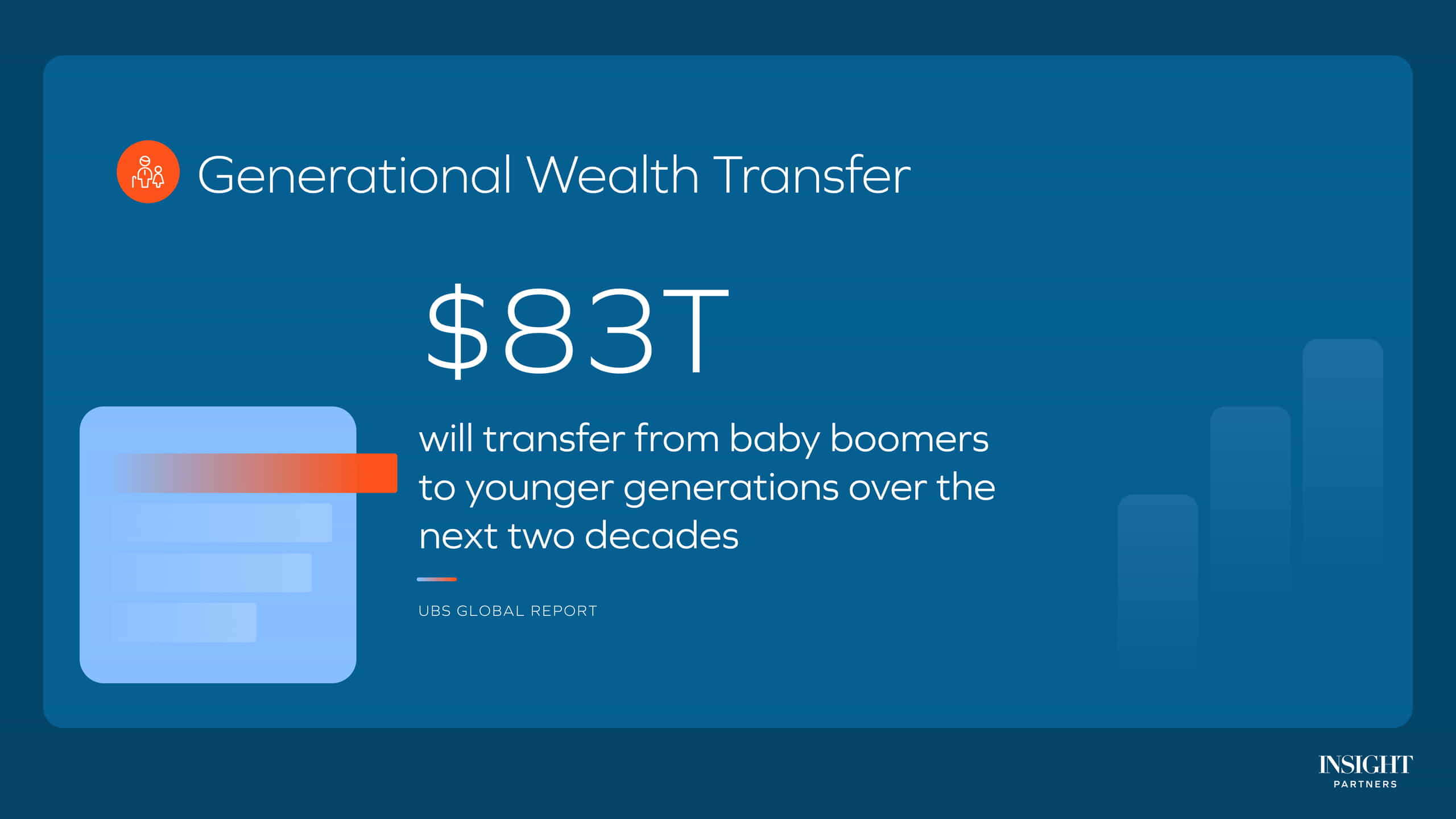

$83 trillion in motion

Over the next two decades, an estimated $83 trillion — more than half of all U.S. wealth — will pass from baby boomers to younger generations. As millennials and Gen Z become the next stewards of capital, expectations around wealth management will change. Clients won’t tolerate cumbersome onboarding, manual data entry, or delayed reporting. At the same time, demand for wealth guidance is high. Over 60% of Americans say they would turn to a financial advisor after receiving a windfall.

Clients expect increased services and personalization

Clients are expecting more from their advisors and want advice to span their full financial picture (i.e., tax strategy, estate and trust, charitable giving, retirement modeling) while remaining tailored to individual goals. And younger clients are used to real-time platforms, intuitive interfaces, and immediate access to information.

“Millennials and the next generation of clients expect and deserve institutional grade guidance with the speed and usability of consumer grade experiences. They won’t settle for anything less.”

— Ross Gerber, CEO of Gerber Kawasaki

A shrinking advisor talent pool

A large share of advisors are nearing retirement, and attracting the next generation is increasingly difficult in a role that demands both technical fluency and relationship skills. By 2034, McKinsey estimates the industry will face a shortage of roughly 100,000 advisors.

“The human piece of financial advice isn’t going away. The right technology just lets our team accomplish more, but the value has to be real.”

— Josh Brown, CEO of Ritholz Management

AI may actually increase demand for financial advisors. Jevons’ paradox states that when technology makes a resource more efficient, demand for that resource increases rather than decreases. As AI boosts advisor productivity, firms will have the capacity to serve segments of the market that were previously too costly or complex. The result isn’t fewer advisors, but more people gaining access to advice they couldn’t afford before.

“By automating admin work, AI allows advisors to spend more time on client relationships and strategic guidance, where they add the most value. This will likely lead to a stronger advisory offering and greater demand for financial advisors, not less.”

— Arthur Ambarik, CEO of Perigon Wealth Management

Consolidation is raising the stakes

RIA M&A is accelerating, raising the technology bar across the market. For independent firms, modern systems are now table stakes to remain competitive against better-capitalized platforms. For aggregators, technology is key for integration and often determines whether a roll-up generates durable value.

“As firms grow larger, having a unified technology experience across the enterprise becomes table stakes. Expectations continue to grow both for us and for our vendors, particularly with accelerated AI development.”

— Stefan Ludlow, CTO at Cerity Partners

Buyers are increasingly scrutinizing technology stacks in diligence, with technology quality directly influencing valuation and integration risk.

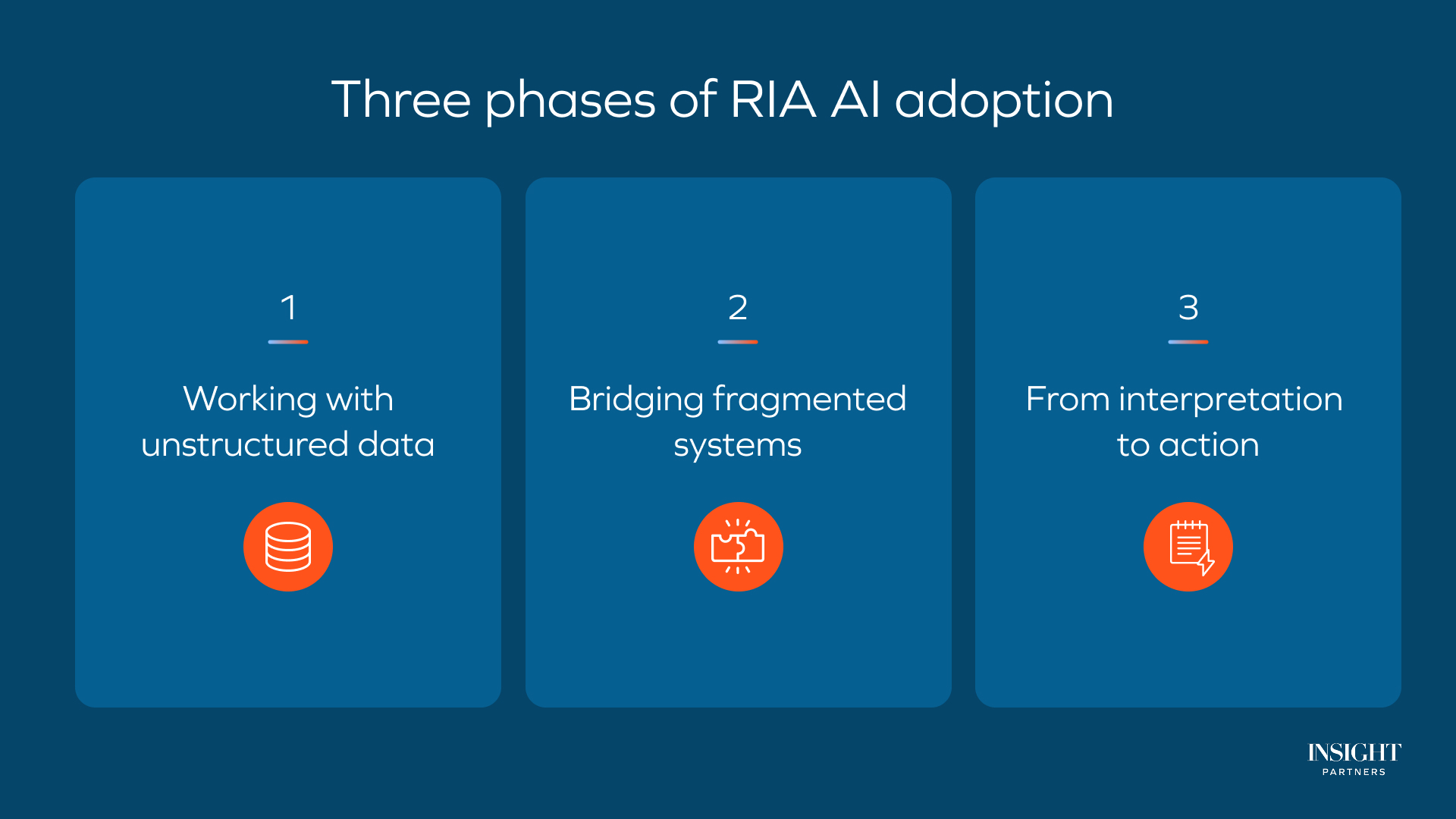

The three phases of AI adoption in wealth management

Wealth management is well-positioned to benefit from AI, and the opportunity will likely unfold in three phases.

Phase one: Making sense of unstructured data

The industry runs on unstructured documents: client agreements, custodian files, account statements, and more. Because unstructured data lacks consistent formats, extracting meaningful information typically requires manual, tedious review. This slows everything from introductory calls to reporting.

“Jump is using AI to turn unstructured meeting conversations into actionable insights — surfacing client sentiment, streamlining prep, and eliminating the admin work that traditionally keeps advisors behind their desks instead of in front of their clients,” says Jump* Cofounder and CEO Parker Ence.

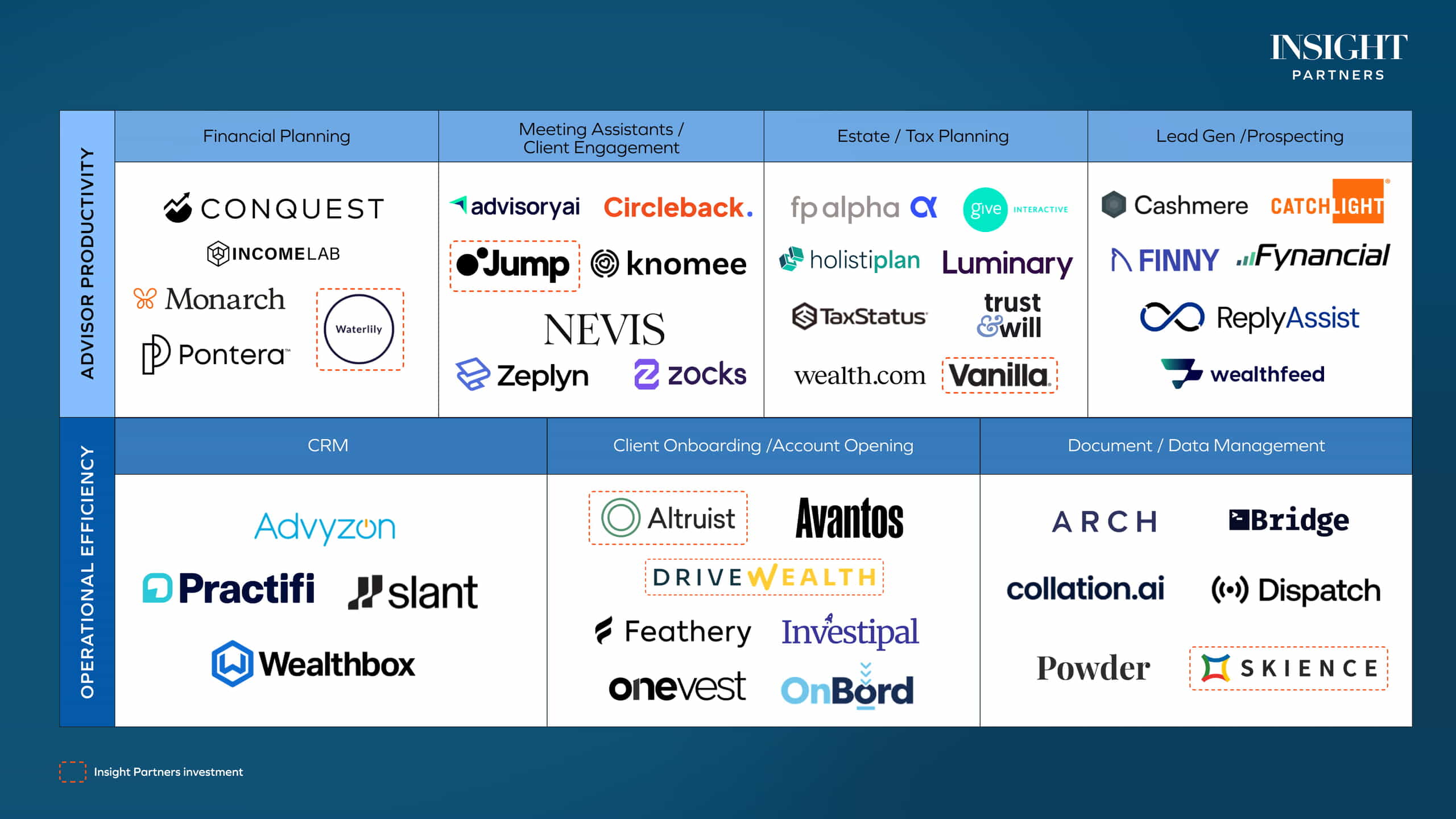

Estate and tax planning have traditionally meant sifting through dense documents and leaning on specialists for interpretation. Now, platforms can extract key clauses, interpret their implications, and make intelligent recommendations aligned with a client’s overall goals — Wealth.com and Vanilla do this in estate planning, and Holistiplan does this in tax.”Vanilla is using AI to read dense documents and extract the information that matters,” says Vanilla* Founder Steve Lockshin.

Phase two: Bridging fragmented systems

Once data is structured, the next challenge is normalizing it across CRMs, portfolio accounting platforms, custodians, and planning tools — each with its own data model and structure. It’s not enough to just organize data; the real value comes from cleaning and validating it along the way. AI can interpret the business context behind data to resolve inconsistencies and unify workflows.

“Wealth managers will move toward a single platform to run their end-to-end processes, and because Altruist controls the custody layer, we can streamline complex operational workflows inside one system,” says Altruist* Founder and CEO Jason Wenk.

CRMs sit at the center of this challenge — it’s where client data either gets unified or stays siloed. Platforms like Practifi, Advyzon, and Slant are evolving beyond traditional contact management to support workflows across systems.

Solving data fragmentation raises the question: Who owns the data layer? We believe that firms should own their data, and that they are right to be wary of companies that make it hard to leave. Startups and ScaleUps should offer value without creating artificial lock-in.

“Data lives across different systems that don’t talk to each other, but that are all integral to creating a comprehensive plan. AI helps bridge that gap by understanding the meaning behind the data, not just the fields.”

— Dimitri Eliopoulos, CEO of Curi Capital

Phase three: From interpretation to action

Once data is in order, firms can effectively use AI to automate workflows. Many processes today remain manual and spreadsheet-based. Once data is unified, AI Agents can support the actual execution of work — automating routine tasks, streamlining data reconciliation, and resolving errors across systems. OnBord and Investipal are streamlining client onboarding: automating document collection, account opening, and custodian submissions that traditionally require advisors to enter the same data across multiple systems.

“We’re moving from AI that understands to AI that does. But these tools have to truly understand the workflows they’re executing.”

— Jonathan Rogers, CEO of Forum Financial

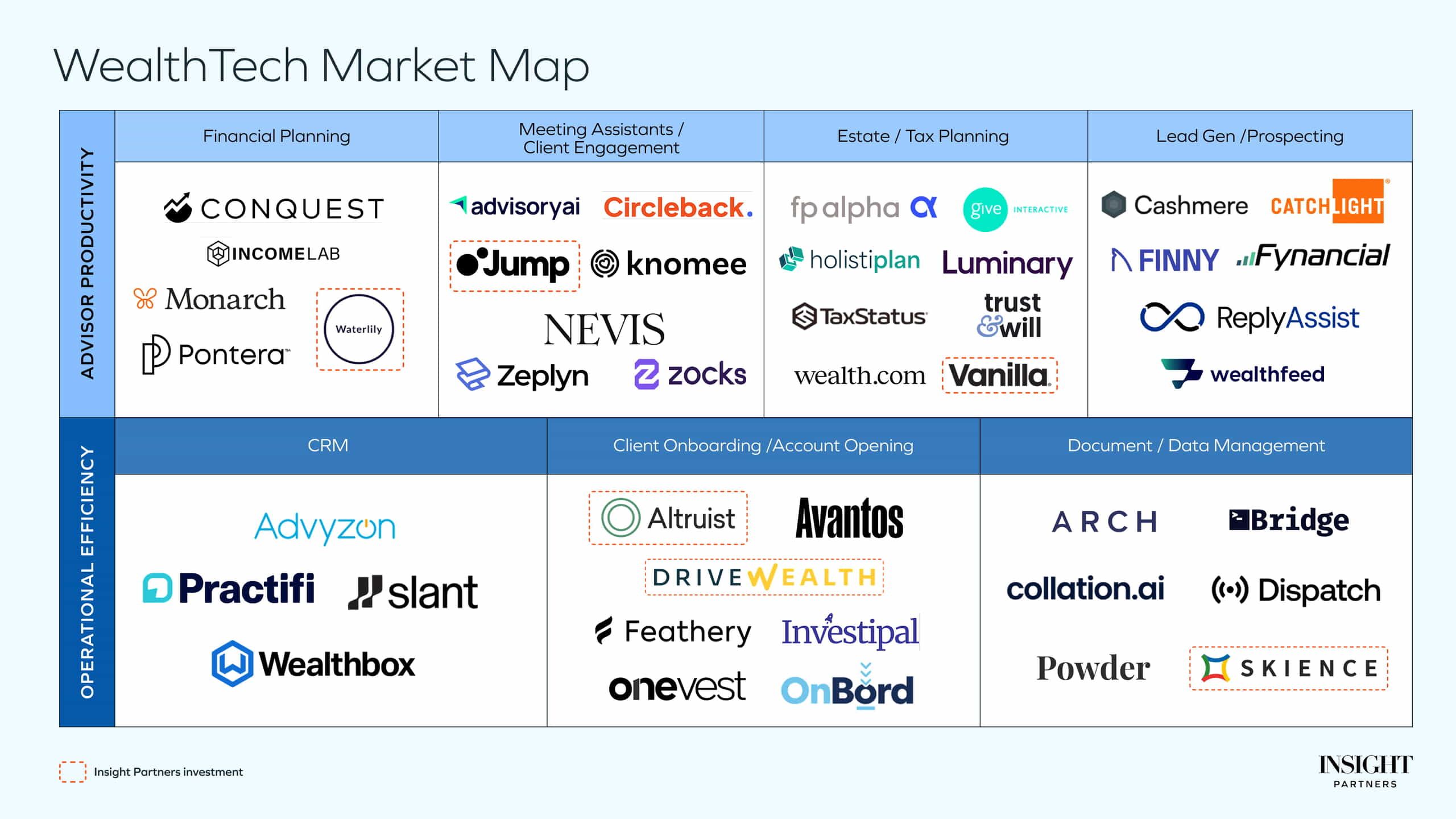

Where WealthTech innovation is happening

While advisors will likely adopt AI in three phases, companies are attacking the opportunity from two directions: front-office tools that help advisors grow, and back-office infrastructure that helps firms scale.

In the front office, advisors are using AI to automate lead identification and outreach. “We’re enabling better outcomes for both the advisors and clients by ensuring an optimal match. RIAs tell Finny the types of clients they serve best, and our AI finds them,” says Finny Cofounder and CEO Eden Ovadia.

Financial planning platforms are enabling advisors to specialize in areas they previously lacked bandwidth to address. Pontera focuses on held-away and retirement accounts, while Waterlilly* tackles long-term care planning.

“We see real potential in AI to help us deliver a better client experience while also reducing some of the manual coordination behind the scenes for our team. Used thoughtfully, these tools can help us grow without sacrificing personalized service.”

— Bryan Zschiesche, Managing Partner of Financial Synergies

Wealth management is heavily regulated, though, which creates a high bar for any AI company. Client data is sensitive, reporting requirements are strict, and mistakes have real consequences. Companies should demonstrate a real understanding of the industry’s cybersecurity and compliance requirements. On top of that, wealth workflows are specific, and integrations are complicated. Generic tools typically can’t handle integrations out of the box, which is why firms are gravitating toward vertical-specific companies.

“Trust is everything in our industry, and there are still a lot of unknowns around AI. That’s why we need wealth-focused solutions for our workflows.”

— Andrew Hart, CEO of Next Capital Management

Reshaping wealth management

We’re still in the early innings of AI in wealth. For RIAs, the question isn’t whether to adopt these tools — it’s where to start and how to sequence. For the startups building in this space, the opportunity is enormous, but earning trust in a regulated, relationship-driven industry takes time. The firms and startups that succeed won’t just grow faster — they’ll reshape what wealth management looks like for the next generation.

If you’re building in the space, we’d love to meet. Email us at earnowitz@insightpartners.com.

*Note: Insight Partners has invested in Altruist, DriveWealth, Vanilla, Waterlily, Skience, and Jump.