Back

Investor POV

De-risking climate change with software: opportunities, challenges, and resources for innovation

Nicole Shimer | November 16, 2023| 12 min. read

As the world confronts the stark realities of climate change and the transition to clean energy accelerates, enterprises must undergo a pivotal shift.

To meet the net zero mandates of regulators and institutional investors, optimize business models, increase shareholder value, or make a positive impact, 66% of the Fortune Global 500 have a significant climate commitment.

The portion of that group actively reducing their reported emissions earned on average nearly $1B more in profit than their peers (YoY), demonstrating that well-run businesses are choosing to follow through on their climate commitments. At the same time, large businesses and governments working toward decarbonization are also being forced to adapt to increasingly extreme weather events.

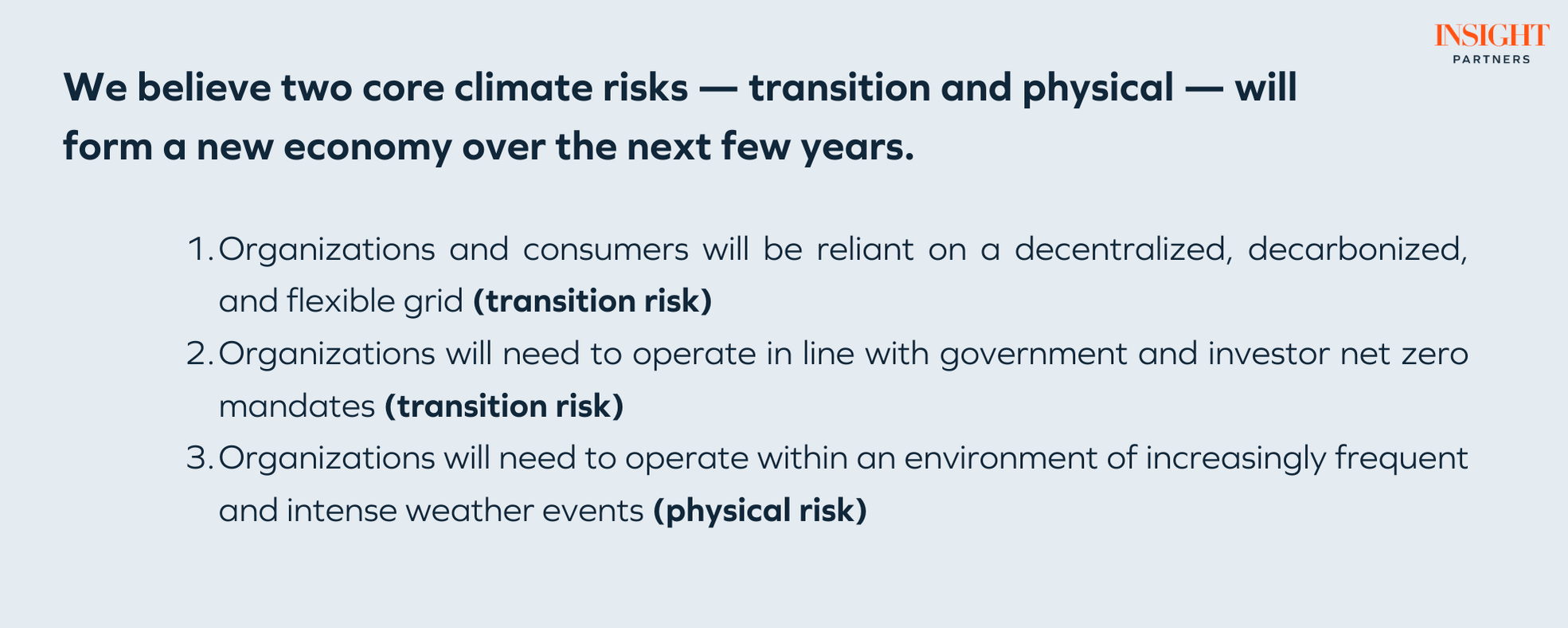

The immediate challenge lies in managing two core climate risks: transition and physical. The former requires adapting to a lower-carbon economy, while the latter deals with the tangible impacts of climate change.

Climate software will play an instrumental role in allowing businesses and governments to adapt and thrive in this new environment. Of course, physical solutions, like electric vehicles, solar panels, more performant batteries, and carbon-sequestering materials will also be vital in tackling the energy challenges ahead of us.

But software can harness the full potential of these physical assets, accelerating our transition to a new, more resilient economy that is inextricably linked with climate change.

The journey towards the economy we describe is a necessary evolution and one of the largest opportunities of this century. We are excited to back the software businesses enabling it.

The industry

Three big shifts illustrate the importance of managing both transition and physical risk in the 21st century and ways to turn those risks into opportunities for innovation and growth:

- The grid transition

- A net-zero economy

- An extreme-weather economy

The grid transition

One reason the clean energy transition is accelerating so rapidly is because it has become an economically viable means of matching increasing energy demand. Between 2010 and 2021, the cost of solar declined by 88%, and onshore wind declined by 68% globally.

Given these drastic price decreases alone, it is no surprise solar and wind will supply over 33% of global power by 2030, up from 12% in 2023.

Let’s consider the situation in the United States as a case study. According to the US Department of Energy’s new report on virtual power plants, between 2023 and 2030, the United States will need to “add enough new power generation capacity to supply over 200 GW of peak demand”.

For context, 200 GW can power all US households, up to 175 million homes, for a full year. We need to meet this supply target in order to prevent power outages during peak demand and maintain reasonable energy costs for consumers.

In addition, according to the US Energy Information Administration (EIA), 42% of grid generation will come from renewable energy in the US by 2050 – a result of lower prices, compliance carbon markets, the White House’s target of eliminating fossil fuels as a form of energy generation by 2035, national energy security, and more.

Therefore, not only does the US need to drastically increase energy supply, it also needs to match that increase with renewable energy, driving many complexities and strains on the grid.

The US has released a large amount of funding to support this massive transition.

- The $396B US Inflation Reduction Act (IRA) is estimated to drive a 40% reduction in climate technology costs, ranging from battery manufacturing to electric vehicle production.

- Coupled with the Bipartisan Infrastructure Investment and Jobs (IIJA) Act ($1.2T over five years) and The Creating Helpful Incentives to Produce Semiconductors and Science (CHIPS) Act ($280B through FY2027) nearly $2T of US government funding will be available from these three federal climate policy packages over the next few years.

However, integrating renewable energy into electrical grids is proving to be one of the biggest challenges of our time. Transmission interconnection backlogs are averaging 5 years. A complex network designed to balance power supply with power demand now additionally has to onboard new types of renewables (hydro, geothermal, etc) and leverage virtual power plants.

This new grid also needs to service explosive electric vehicle growth – EVs will be 18% of the overall car market in 2023, up from 4% in 2020. Software will play a vital role in the transition toward a more decarbonized, decentralized, and flexible system.

A net-zero economy

Over 76% of global emissions are from jurisdictions with net zero targets, including the United States, the European Union, and China. This drive to decarbonize is upping the demand for better climate data analysis and reporting as regulations are passed to help meet these goals.

The compliance carbon market ($909B in 2022) includes 28 official Emissions Trading Schemes (ETSs) in operation globally, including the EU’s and California’s, covering about 17% of global emissions. Power generation and energy-intensive industries subject to an ETS are already paying for their emissions.

Beginning October 2023, the EU’s Carbon Border Adjustment Mechanism (CBAM) will go live with reporting mandates: the world’s first climate border tax. By 2026, foreign companies will have to pay a tariff in line with the EU’s carbon prices if they export goods into Europe, potentially netting the EU $80B a year by 2040.

What’s more, the EU’s Sustainable Finance Disclosure Regulation (SFDR) already mandates that all financial market participants and financial advisers with more than 500 employees based in the EU publish firm-level sustainability disclosures.

The upcoming European Sustainability Reporting Standards (ESRS) will require thousands more EU companies to make ‘double materiality’ assessments, and report both on how their business is impacted by sustainability issues and how their activities impact society and the environment.

While the SEC’s upcoming climate disclosure rules have not been finalized yet, California lawmakers passed the first US mandatory emissions disclosure bill in September 2023 which should require about 5,000 companies earning over $1B annually to report not only their direct emissions, but also their Scope 3 or indirect emissions (i.e. coming from employee business travel or upstream supply chain activities).

While regulations are critical, they are often delayed or changed. Therefore, it is equally important to consider how businesses and investors are ensuring their suppliers or portfolio companies decarbonize and report on their emissions for bottom-line-driven incentives.

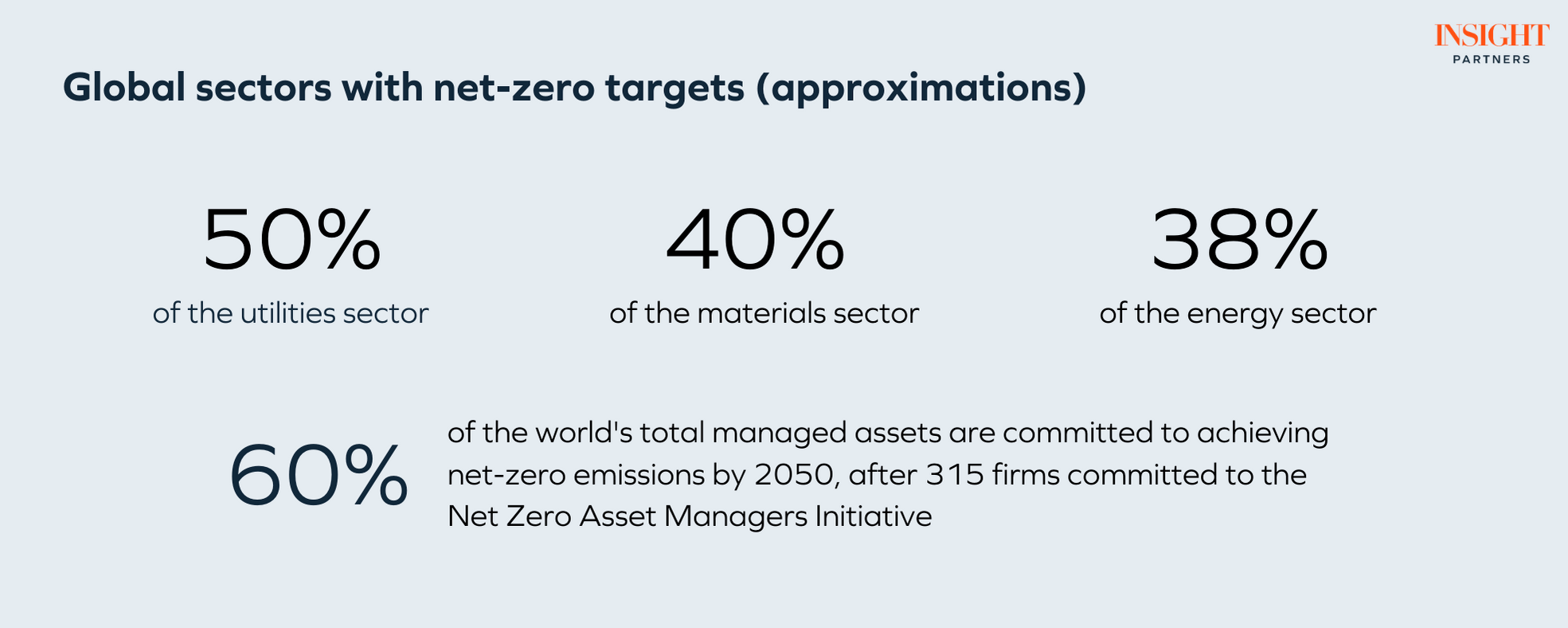

As of Q2 2023, about half of the utilities sector globally has set net-zero targets, followed by 40% of the materials sector and 38% of the energy sector. BlackRock and over 300 firms representing $64T in AUM have committed to the Net Zero Asset Managers Initiative, meaning about 60% of the world’s total managed assets are committed toward achieving the goal of net-zero emissions by 2050 or sooner.

Walmart, Sephora, and Apple are a few examples of enterprises choosing suppliers based on clean energy initiatives. For example, Apple recently announced that 300 suppliers comprising over 90% of their direct manufacturing spend “are committed to using 100% renewable electricity for all Apple production by 2030.” As of 2022, Apple had already achieved carbon neutrality and reduced emissions by 45% since 2015.

The demand for software that can assist businesses and governments in meeting their targets will only increase.

An extreme weather economy

Even if the world rallies and we achieve the lowest greenhouse gas (GHG) emissions scenario possible, global warming will continue to increase through 2040, past the +1.5°C tipping point set by The Paris Climate Agreement, according to the most recent IPCC report.

This means we will have increases in heat-related human mortality; food-borne, water-borne, and vector-borne diseases; extreme weather including heavy precipitation; flooding; and wildfires.

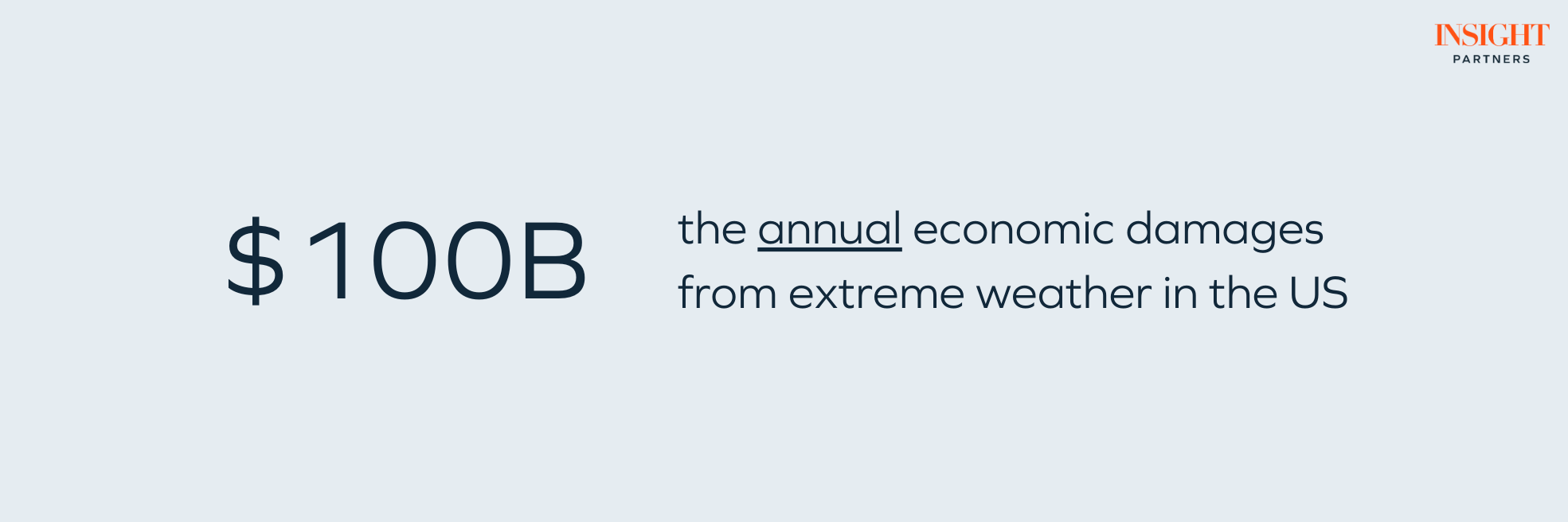

The drastic implications are already playing out in the insurance industry. This summer, as a result of increasing wildfires and flooding, both State Farm and Allstate fully pulled out of offering insurance in California for new homeowners and businesses. Louisiana and Florida are also in the midst of insurance crises given rapid increases in hurricanes and flooding.

Any business with a significant supply chain is also at risk. According to a Harvard Business Review study analyzing the supply chains of 100 original equipment manufacturers (OEMs) in the high tech, auto, and consumer goods industries, 93% of suppliers in China and Taiwan had major increases in climate variability over the past two decades and nearly half of these suppliers “have either no business continuity plans or no alternative sites lined up that could be put into operation quickly.”

Only 11% of all supply chain sites in the three countries studied – the US, China, and Taiwan – were fully prepared for climate-related disruptions.

When governments invest in disaster mitigation, communities are better protected from deaths, infrastructure damage, disease, violence, and business closures, to name a few.

Extreme weather combined with a stressed grid, a situation in which society faces transition risks and physical risks at the same time, is particularly deadly; during a power outage in NYC during a heat wave in 2003, there was a 313% increase in respiratory-related hospitalizations and a 32% increase in deaths compared to a standard day. This resulted largely from residential medical equipment being unable to be charged, a lack of air conditioning, and isolation due to elevators and subways not functioning properly.

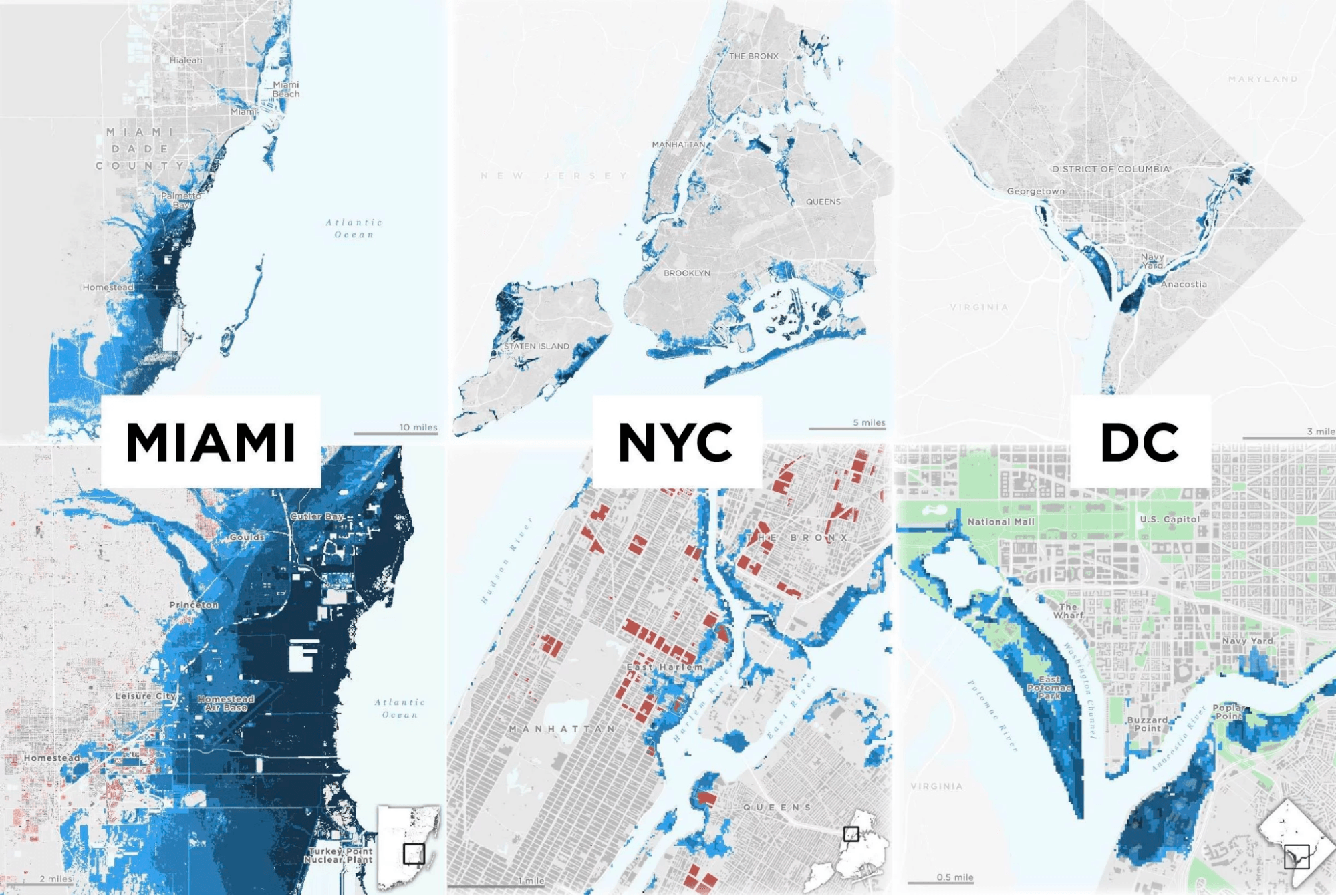

The future impact of hurricane flooding on US cities based on modeling from the National Hurricane Center. Future sea rise alone could expose about 720,000 more people to flooding in these cities. Credit: NPR.

The demand for software that can help businesses and governments predict weather events and potential subsequent damage will only increase in parallel to climate change.

The investment landscape

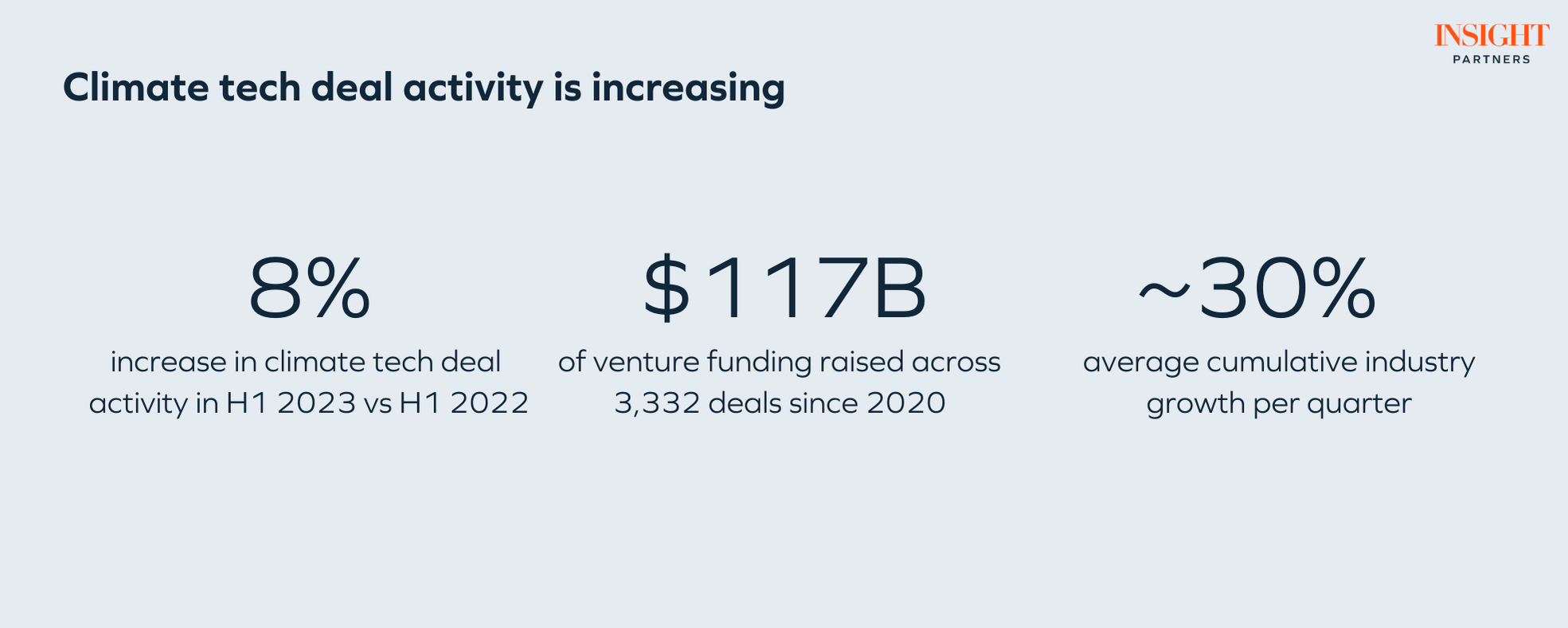

Despite the current challenging market environment, the climate tech sector has shown remarkable resilience. In 2022, climate tech companies raised $40B, and there were 140 exits – a 70% YoY increase. In Q1 2023, climate tech represented ~20% of global tech funding.

According to CTVC, climate tech deal activity increased by 8% in the first half of 2023 (compared to the same time period in 2022) despite the 53% decrease in overall venture investing. Taking a step back, since the start of 2020, ~2,500 climate tech companies have raised $117B of venture funding across 3,332 deals, with cumulative industry growth averaging ~30% each quarter.

Given the rapidly evolving and nascent subsectors within climate tech, data around investments for software-only solutions can be hard to find. However, according to a recent Lazard report, climate software private investments grew ~3x the rate of other climate tech business models in 2022. Lazard also found that climate tech software investments specifically targeting the energy sector increased 77% YoY.

One key area investors look toward to validate large investments is TAM size, which is particularly important for emerging categories. The climate tech TAM today is valued over $20B, and is expected to grow by a compound annual growth rate (CAGR) of 24.5% from 2023 to 2033.

Within that, the global market for SaaS-based energy technologies is projected to grow from $3.5B in 2021 to $17.5B in 2030, at a CAGR of 19.7%.

McKinsey’s projections further validate these market sizes, highlighting the emergence of six $100B+ value pools across carbon management, waste, agriculture, consumer, power, and buildings by 2030.

The opportunities

Given Insight’s unique ability to invest across stages with various ownership structures, we have specific theses around climate investments that range from $10-$15M Series A deals to $100M+later-stage growth and majority deals – and everything in between.

In the early stage space, where buyers are typically still early in the adoption curve, we are seeing numerous greenfield climate categories rapidly growing across enterprise software, where first-mover leaders are emerging as critical market infrastructure.

Sylvera, for instance, a first mover in carbon market monitoring and ratings, has quickly anchored itself as a key player, forming partnerships with Bain, McKinsey, S&P, and Salesforce. Similar opportunities exist in virtual power plants, weather impact monitoring and response, and electric vehicle fleet management.

Many of these companies grow from under $1M ARR to becoming the gold standard in their specific field within a few years, given how new and mission-critical many climate categories are.

In the later-stage space, buyers and the market have matured, with many established companies having enough revenue and cash flow for $100M+ equity deals. Notably, half of the $40B poured into climate tech in 2022 went into post-Series D rounds.

Strategic climate tech acquirers with large pockets are already active across big tech, energy, and financial services, ranging from Shell and Schneider Electric to Google and Nasdaq. A growing portion of the massive annual energy and utility spend goes toward software solutions supporting the grid transition.

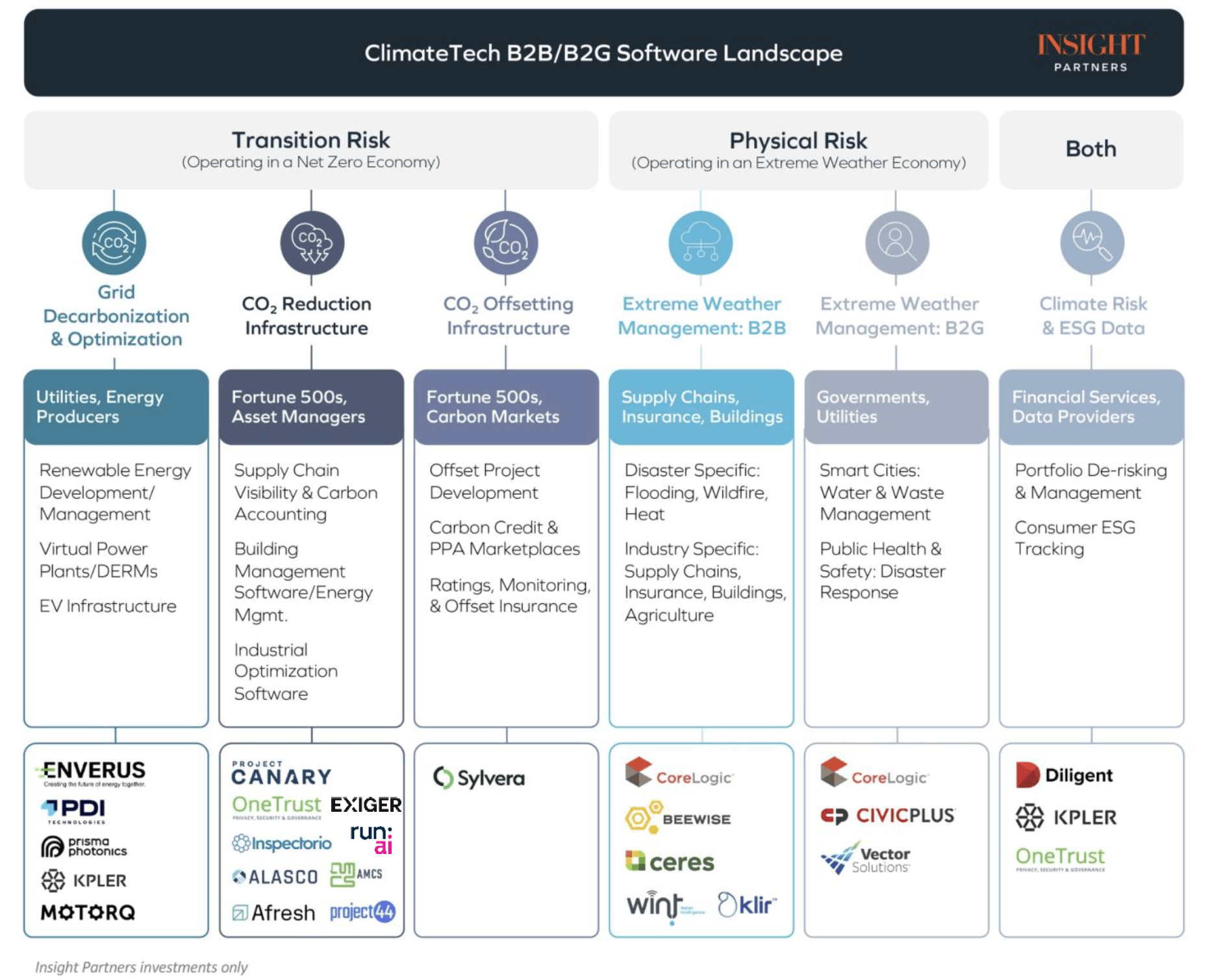

Within this wider market context, there are four particularly important opportunities where we see immense potential for early to late-stage investments:

- Grid decarbonization and optimization

- CO₂ reduction and offsetting infrastructure

- Extreme weather management (B2B & B2G)

- Climate risk and ESG data

Grid decarbonization and optimization

As renewable energy production scales up, the energy landscape is shifting toward a decentralized network of many smaller producers (ranging from utility-scale to residential). This new ecosystem will require distributed energy resource management systems (DERMS) and virtual power plants (VPPs) to support existing energy producers in maintaining the grid.

It will also require electric vehicles to be seamlessly integrated into the grid, which means including vehicle to grid (V2G) technology. V2G allows EVs to become their own batteries and redistribute energy back to residences or the grid during peak demand.

In addition, there will be increasing demand for aggregated APIs for DERs. Currently, companies that want to tap into this new ecosystem have to navigate various API types and security protocols to establish each connection. They need software that simplifies connectivity and reduces development overhead.

CO₂ reduction and offsetting infrastructure

To combat climate change, enterprises across all industries, from automotive to agriculture, need to 1) reduce the carbon footprint of their operations and 2) offset unavoidable emissions.

Businesses will need supply chain visibility and carbon accounting software to gain insight into their emissions data and measure their progress towards carbon neutrality, as well as industrial optimization to pivot to greener operations. For example, buildings should optimize their HVAC systems to minimize energy use, saving energy costs and excess emissions.

Any business with a significant supply chain should be tracking how shifting to recyclable materials or less carbon-intensive materials could improve sales, reduce costs, and help comply with regulations.

The voluntary carbon market (VCM) helps enterprises and governments offset unavoidable emissions through nature or technology-based solutions that remove carbon from the atmosphere. These projects range from reforestation to direct air capture (DAC) technology and need to be measured, reported, and verified using software to track successful emissions reduction.

Compared to ‘insetting,’ where enterprises try to remove emissions leveraging their existing supply chain, offsets can be formally diligenced by entities that are incentivized to prevent greenwashing. We are bullish on the VCM.

Software solutions are vital in building and scaling trusted carbon markets and renewable energy markets to give enterprise buyers full confidence to make investments. Specific examples include power purchase agreement (PPA) marketplaces and insurance for carbon offset project buyers to reduce failed delivery risk.

Extreme weather management (B2B & B2G)

The increasing climate volatility is putting trillions of dollars of assets at risk. Governments, businesses, especially those with large supply chains, insurers, and building management companies, will increasingly need software to assess and price the physical risk of extreme weather events. They also need software to manage extreme weather’s inevitable impact – both for long-term planning and immediate response.

Some scaleups specialize in offering tailor-made solutions for specific disasters, like simulation modeling, risk analysis, and operational response for wildfires. Others carve a niche in a specific industry, like supply chains, insurance, building management, agriculture, or water and waste management for smart cities. All are critical.

Climate risk and ESG data

Quality data, or the lack thereof, remains a significant ESG challenge facing boards, financial institutions, and investors. Software that bridges this gap, standardizing and streamlining ESG data analysis and reporting, will be paramount.

Some examples of where ESG data is critical is enabling the development and sale of green bonds or creating ESG-focused ETFs. Hedge funds may track ESG signals in real time as a negative ESG signal, like reports of greenwashing, can quickly materially affect stock prices.

Overall, tools that accurately quantify environmental performance will be in demand as owners and investors seek to de-risk their portfolios, prioritize greenhouse gas emissions reduction, and adapt to a global economy that is moving toward net zero.

The innovators

Several companies are already helping businesses and governments manage their physical and transition risks and are becoming critical parts of the climate tech ecosystem.

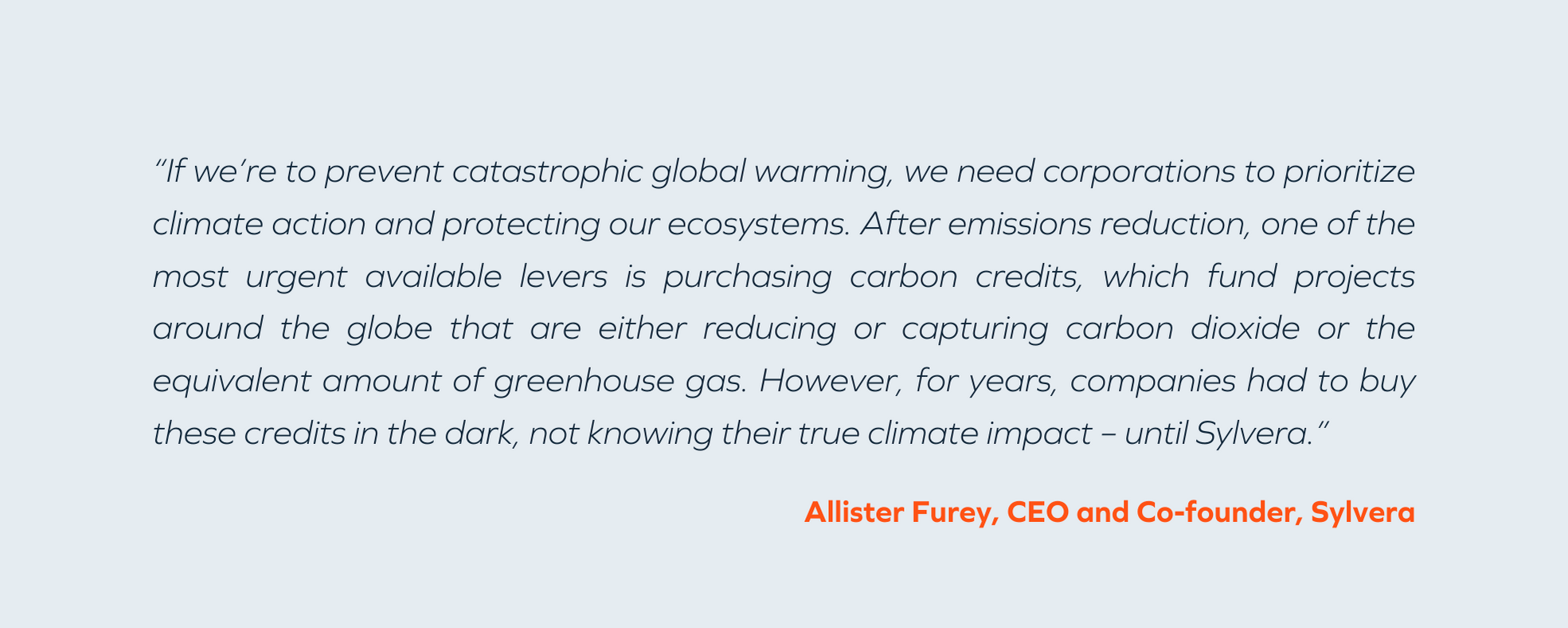

Sylvera

Sylvera’s mission is to be a source of truth for carbon markets. To help organizations ensure they’re making the most effective investments toward net zero, Sylvera builds software that independently and accurately automates the evaluation of carbon projects that capture, remove, or avoid emissions. With Sylvera’s data and tools, businesses and governments can confidently invest in, benchmark, deliver, and report real climate impact.

Sylvera has quickly cemented itself as the go-to solution for managing Fortune 500’s carbon offset portfolios. Today, more than 50% of nature-based offsets are traded on a venue, by a trader, or bought by a buyer where Sylvera data is displayed or accessed.

Project Canary

Project Canary provides comprehensive environmental data and software solutions to help utilities and oil and gas companies measure, analyze, and improve their environmental performance, reduce their carbon footprint, and mitigate climate impacts.

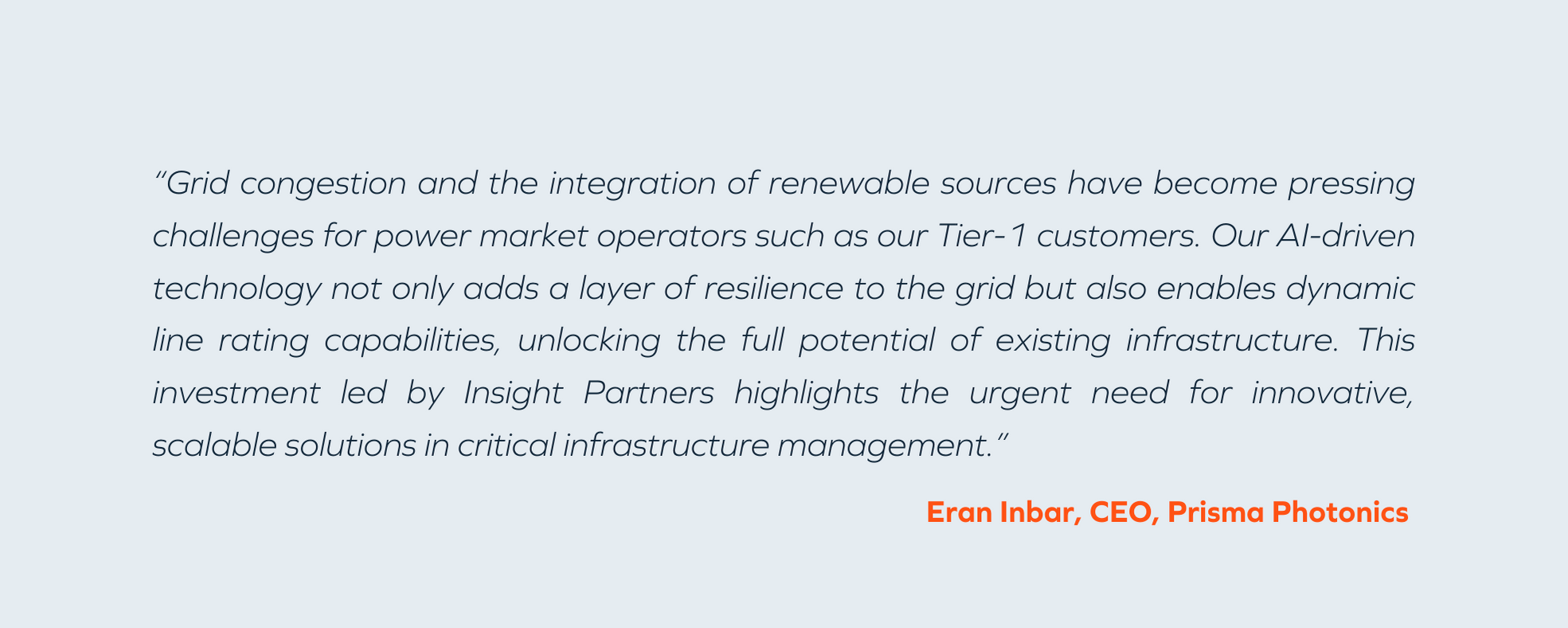

Prisma Photonics

Prisma Photonics solutions monitor and manage large-scale infrastructure such as power transmission grids, oil and gas transmission pipelines, long-spanning railways, highways, subsea cables and pipes, and more.

Its fiber sensing technology offers safer, secure, efficient, and cost-effective operations while protecting the environment by preventing spills, wildfires, and other environmental hazards.

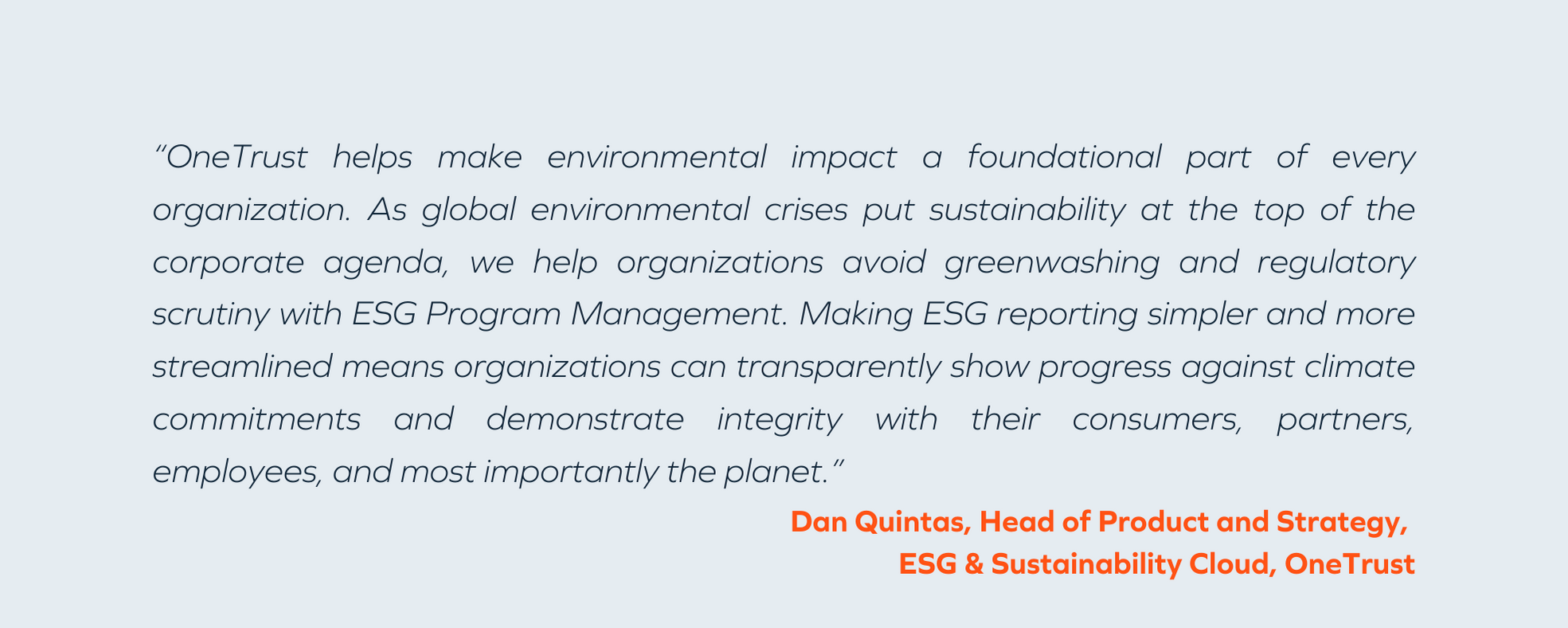

OneTrust

OneTrust is the fastest-growing and most widely used technology platform to help organizations be more trusted and operationalize privacy, security, data governance, and ethics and compliance programs.

As investors, employees, and regulators expect organizations to act sustainably, reduce carbon emissions, and make meaningful climate impact, OneTrust helps businesses set climate goals, measure, and reduce their carbon footprint, and manage ESG initiatives.

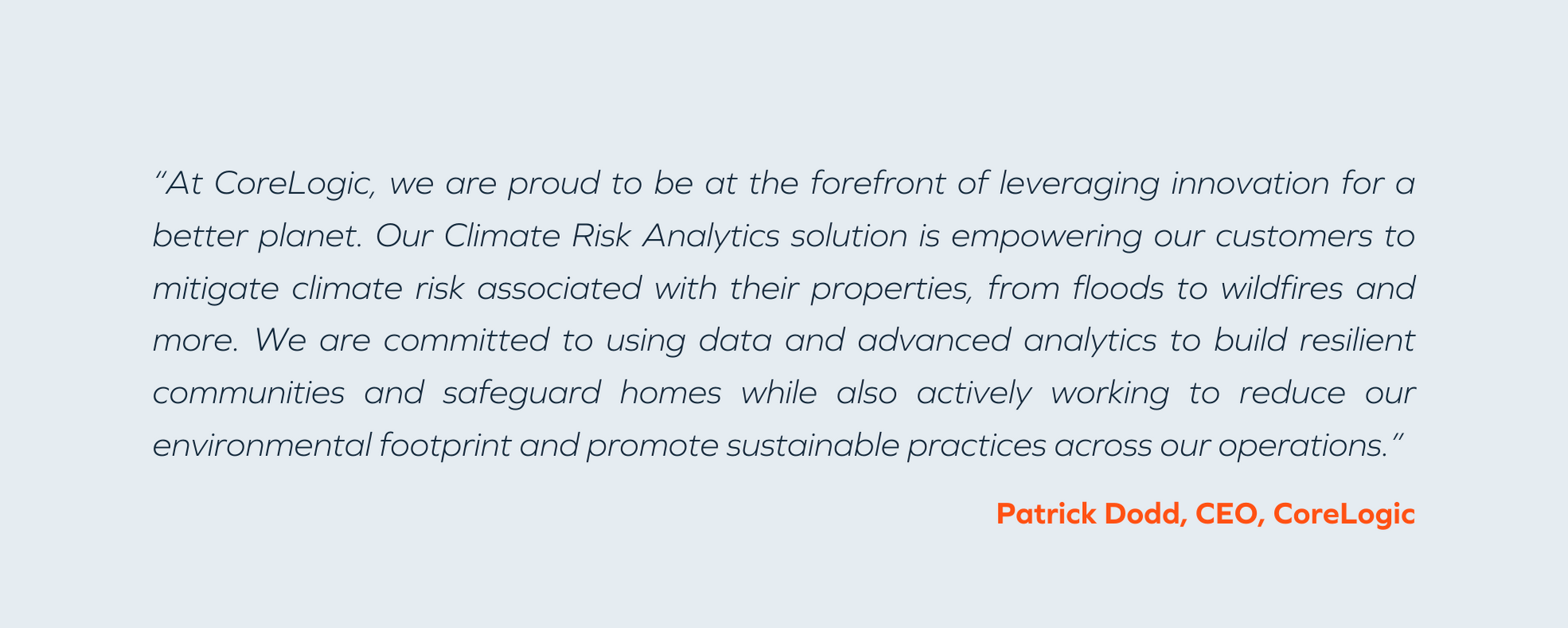

CoreLogic

CoreLogic is a leading provider of property insights and solutions. Its Climate Risk Analytics product combines its industry-leading property data with replacement costs, valuation elements, and natural hazard information to build a comprehensive account of physical climate risk.

Its proprietary climate models calculate the likelihood of what can happen and where so businesses can protect their property, prepare accurate climate compliance, and lessen the impact on their bottom line.

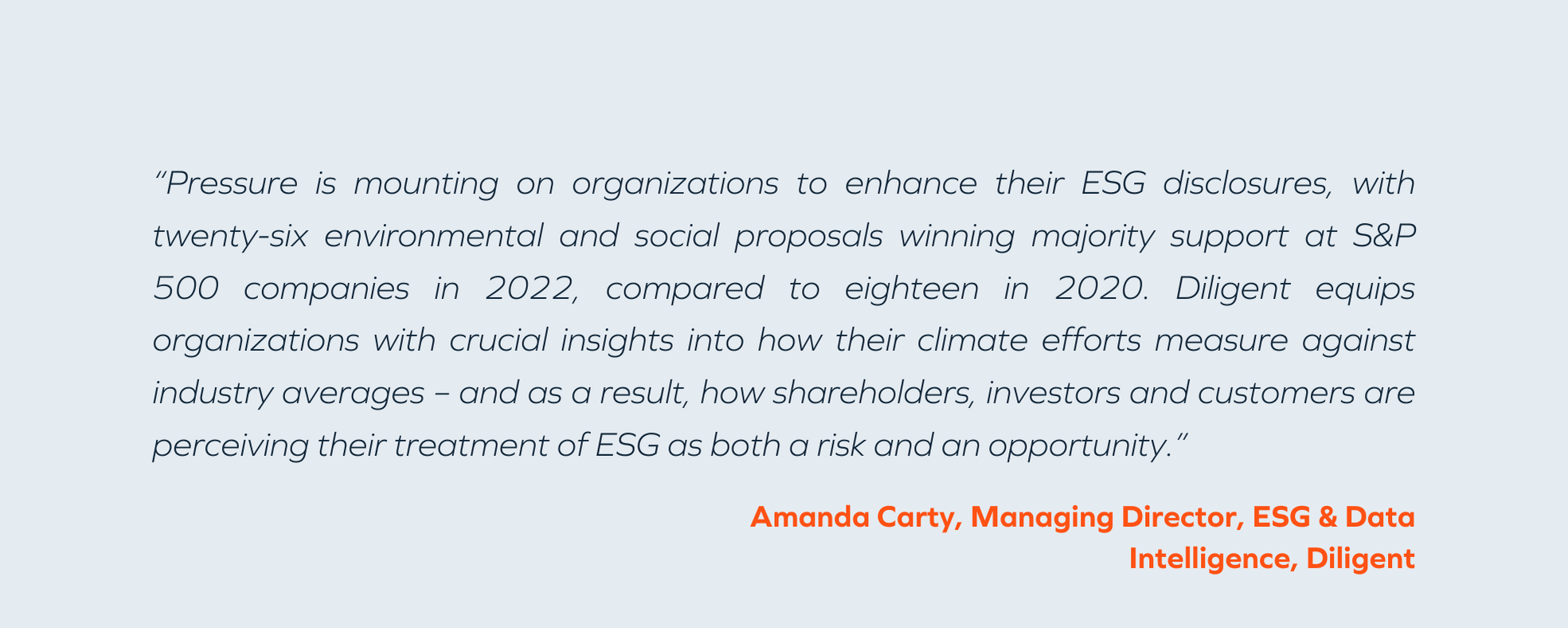

Diligent

Diligent is the pioneer of modern governance, empowering leaders to turn effective governance into a competitive advantage. It provides solutions to streamline ESG board reporting, help companies understand the impact of climate change on governance, and provide clear and consistent insight into climate performance.

The considerations

Here are Insight’s key considerations for founders building a climate software business.

Balancing regulation and innovation

While regulation can offer early momentum for user acquisition, it shouldn’t be the lynchpin of a business model. The potential for regulatory shifts requires climate software companies to build a defensible value proposition independent of regulatory mandates and subsidies.

We look at customer ROI outside of just regulatory compliance for many of our early-to-growth-stage deals in particular.

Navigating budgetary constraints

Climate software companies should tap into businesses’ operational expenditures to avoid being confined to limited sustainability or experimental innovation budgets.

A solution that replaces these costs, especially by streamlining workflows and driving revenue, positions itself for a faster sales cycle and achieves stronger retention by demonstrating tangible ROI.

Attracting the best talent

One of the misconceptions in the industry is the lack of talent. But an increasing number of people working in Silicon Valley and other established tech hubs are joining or starting climate software companies, particularly after Covid, which nudged many to pursue work in more mission-driven industries.

87% of Gen Z professionals would consider quitting a current job if the values of a new company aligned more closely with their own. This is particularly true for the enterprise software segment of climate tech, where the skills and go-to-market strategy are broadly similar.

Considering legacy tech’s unfair advantage to build

Insight has many software portfolio companies that are primarily focused on governance; environment, health and safety (EHS); or supply chain management but have been pulled into adding climate tech features by their customers.

Similarly, consultancies like Bain, BCG, and McKinsey have moved to rapidly address their customers’ climate concerns. While some features might be easy to add, there are more complex challenges that legacy tech companies or consultancies can’t address quickly or cost-effectively on their own. This is where partnerships with specialized climate tech startups become crucial.

Indeed, the majority of climate software exits in 2022 were strategic mergers or acquisitions where legacy businesses, like big energy companies or tangential software companies, needed to buy climate tech capabilities. Shell, BP, Xpansiv, Schneider Electric, Nasdaq, and BlackRock have all been actively acquiring climate software and hardware businesses in the last few years, each making at least three such acquisitions since 2020.

Businesses and governments need climate software to transition into, and continue to thrive in, this clean-energy, net-zero environment, all while mitigating the unavoidable physical effects of climate change.

The resources

If you want to learn more, here are some resources our team and founders recommend.

Newsletters

- US: Climate Tech VC’s newsletter run by Sophie Purdom and Kim Zou

- EU: ClimateU’s Last Week in Climate run by Tim Steppich

Podcasts

- My Climate Journey. Deep-dive conversations with science, technology, and climate leaders. From the MCJ Collective.

- Catalyst. Investor Shayle Kann discusses the world of climate tech with prominent experts, investors, researchers, and executives.

- Watt It Takes. Tells the stories of founders that are making a zero-carbon future a reality. Hosted by Powerhouse Ventures Managing Partner Emily Kirsch.

Market maps

- Voyager Ventures: Electrons for Tomorrow

- Fidelity International Strategic Ventures: Diving into the Climate Fintech Landscape

- Energize Capital: Introducing Electrifying Everything: 2023 Edition

- Contrary Research: Living Landscape: Climate Tech

- We also love all content put out by our friends at Voyager Ventures, Lowercarbon, and Energy Impact Partners, to name a few.

Networks and communities

- MCJ Collective. An early-stage climate tech fund and a community powering collective innovation for climate solutions.

- OpenAir Collective. A volunteer-led, global network accelerating carbon removal advancement and evolution through member initiated missions.

- Work on Climate. The world’s largest and most active climate community, helping to shift talent into climate tech.

- DER Task Force. A community for distributed energy resource enthusiasts.

- AirMiners. A community for people who want to start a carbon removal company.

- Volta Foundation. A global community of 50,000 battery professionals. You can join their Battery Street Slack community here.

- VOYAGERS. A diverse, international community of mission-led people using technology to confront climate-related challenges.

If you are a founder or exploring ideas in this space, we’d love to hear from you at mgoldberg@insightpartners.comand nshimer@insightpartners.com.

Note: Enverus, PDI, Kpler, Prisma Photonics, Motorq, Project Canary, OneTrust, AMCS, Inspectorio, Project44, Afresh, Alasco, Sylvera, CoreLogic, Beewise, Klir, Wint, Ceres, CivicPlus, Vector Solutions, Diligent are all Insight investments.