Go to home page

main-logo

main-logo

Why Insight?

Portfolio

Team

Ideas

Events

Go Login

main-logo-solid

Why Insight?

Portfolio

Team

Ideas

Events

Go Login

twitter

linkedin

instagram

©2026 Insight Partners

ScaleUp Reports

Stories

Industry Insights

Growth Strategies

Browse All

search

Ideas

Insight Onsite

A day in the life: How four companies run FDE motions

Keep reading

Founder and leadership stories

Leadership

CEO Jan Inge Pedersen on building Kabal into an industry-defining logistics platform

Article

Stories

Energy & Climate

Insight Partners

play

Leadership

How Healthie is building the critical infrastructure behind accessible, longitudinal care

Article

Video

Stories

BioTech/Therapeutics

Healthcare

Insight Partners

play

Leadership

How Assured is building the automation layer for healthcare administration

Article

Video

Stories

AI/ML Ops

BioTech/Therapeutics

Healthcare

Insight Partners

Leadership

CEO Jan Inge Pedersen on building Kabal into an industry-defining logistics platform

Article

Stories

Energy & Climate

Insight Partners

play

Leadership

How Healthie is building the critical infrastructure behind accessible, longitudinal care

Article

Video

Stories

BioTech/Therapeutics

Healthcare

Insight Partners

play

Leadership

How Assured is building the automation layer for healthcare administration

Article

Video

Stories

AI/ML Ops

BioTech/Therapeutics

Healthcare

Insight Partners

How Insight Partners is thinking about FDEs

Article

Demystifying the forward deployed engineer

Thought Leadership

Industry Insights

AI/ML Ops

Santosh Iyer, Samma Hafeez, Insight Onsite

Insight Onsite

A day in the life: How four companies run FDE motions

Blog

Article

Growth Strategies

Santosh Iyer, Samma Hafeez

Article

How companies are building and scaling the FDE bench

Growth Strategies

AI/ML Ops

Santosh Iyer, Samma Hafeez, Insight Onsite

Article

Demystifying the forward deployed engineer

Thought Leadership

Industry Insights

AI/ML Ops

Santosh Iyer, Samma Hafeez, Insight Onsite

Insight Onsite

A day in the life: How four companies run FDE motions

Blog

Article

Growth Strategies

Santosh Iyer, Samma Hafeez

Article

How companies are building and scaling the FDE bench

Growth Strategies

AI/ML Ops

Santosh Iyer, Samma Hafeez, Insight Onsite

AI, Agents, and autonomation

Article

How companies are building and scaling the FDE bench

Growth Strategies

AI/ML Ops

Santosh Iyer, Samma Hafeez, Insight Onsite

Article

Demystifying the forward deployed engineer

Thought Leadership

Industry Insights

AI/ML Ops

Santosh Iyer, Samma Hafeez, Insight Onsite

play

ScaleUp:AI

From software to hardware: Where Nest founder Tony Fadell thinks AI will go next

Article

Thought Leadership

Video

Insight Partners

play

ScaleUp:AI

How agentic AI is rearchitecting enterprise workflows

Article

Thought Leadership

Video

AI/ML Ops

Insight Partners

Article

How companies are building and scaling the FDE bench

Growth Strategies

AI/ML Ops

Santosh Iyer, Samma Hafeez, Insight Onsite

Article

Demystifying the forward deployed engineer

Thought Leadership

Industry Insights

AI/ML Ops

Santosh Iyer, Samma Hafeez, Insight Onsite

play

ScaleUp:AI

From software to hardware: Where Nest founder Tony Fadell thinks AI will go next

Article

Thought Leadership

Video

Insight Partners

play

ScaleUp:AI

How agentic AI is rearchitecting enterprise workflows

Article

Thought Leadership

Video

AI/ML Ops

Insight Partners

Investor POV

Investor POV

How AI is rebuilding America’s primary care system

Article

Thought Leadership

Industry Insights

Healthcare

Aayush Setty, Maggie Morse, Jeff Horing, Rob Epstein, M.D.

Investor POV

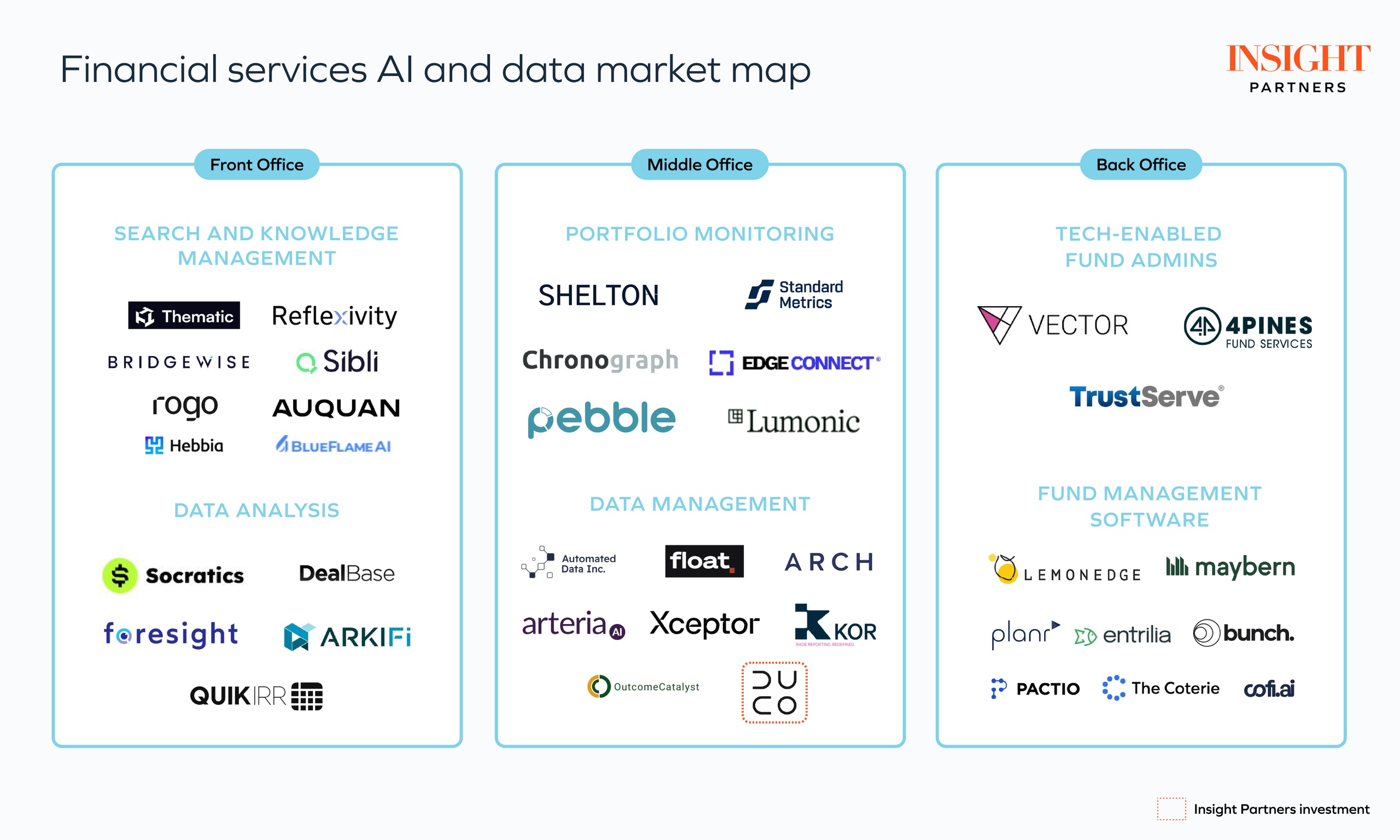

AI in financial services is here: How firms are adopting and where they’re stuck

Article

Thought Leadership

Market maps

Industry Insights

BioTech/Therapeutics

Finance & Accounting

Elan Arnowitz, Alessandro Luciano

Market maps

The state of the robotics ecosystem: The tech, use cases, and field deployment

Thought Leadership

Industry Insights

AI/ML Ops

Lonne Jaffe

Investor POV

Primed for reinvention: Video intelligence industry moves to the cloud

Blog

Article

Thought Leadership

Industry Insights

IT Mgmt

Arjun Mehta, Apoorva Goyal, Alex Debayo-Doherty

Investor POV

Financial services has a data problem: How AI is fueling innovation

Thought Leadership

Industry Insights

Finance & Accounting

Nicole Shimer, Elan Arnowitz

Investor POV

The next industrial revolution: How software is shaping the future of production

Thought Leadership

Industry Insights

Supply Chain & Logistics

Arjun Mehta

Investor POV

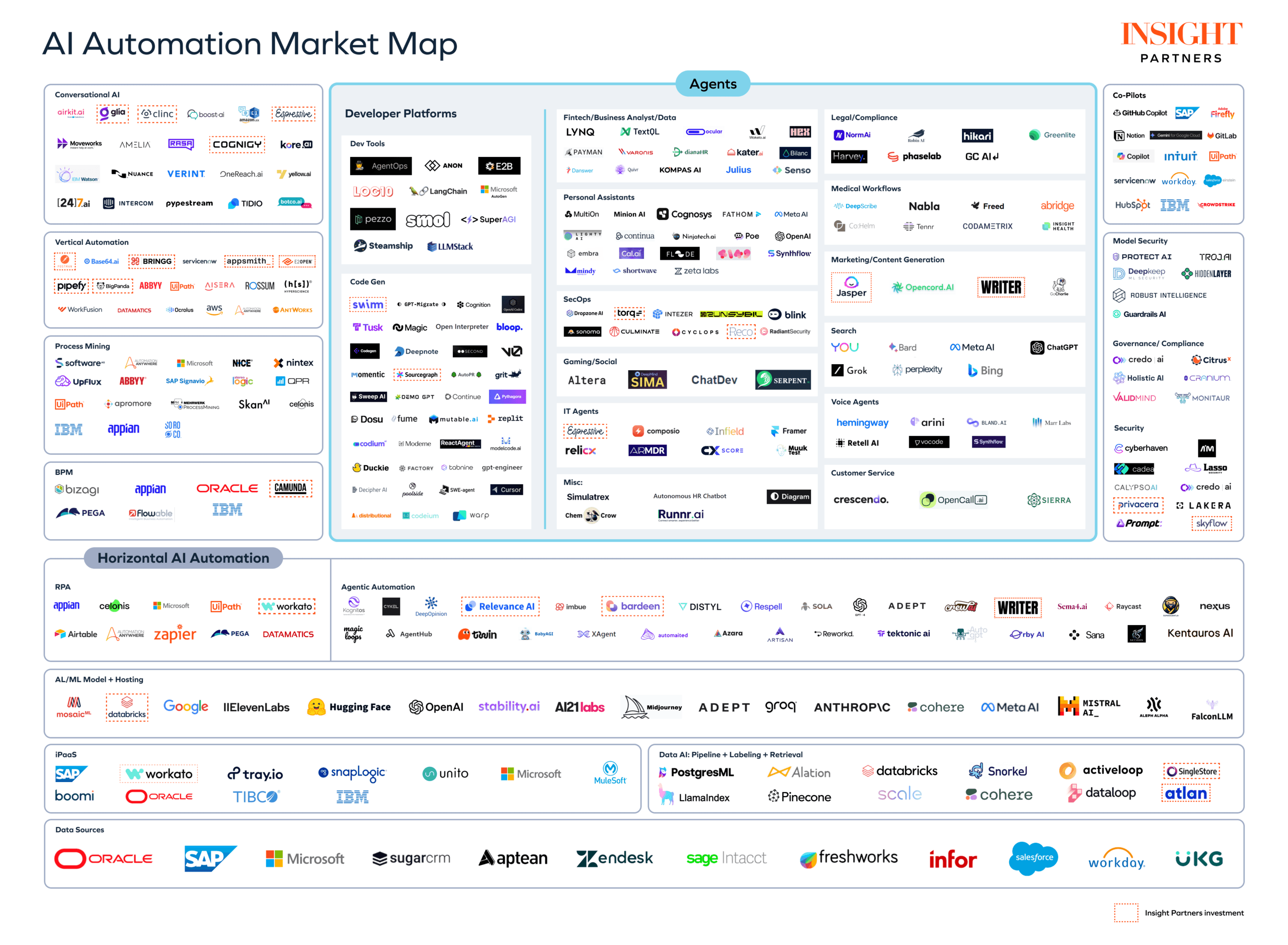

AI Agents are disrupting automation: Current approaches, market solutions and recommendations

Industry Insights

AI/ML Ops

Praveen Akkiraju, Sophie Beshar, Hunter Korn

Investor POV

Investors and CEOs need a climate risk strategy now more than ever. Here are 5 reasons why.

Industry Insights

Deven Parekh

Investor POV

How AI is rebuilding America’s primary care system

Article

Thought Leadership

Industry Insights

Healthcare

Aayush Setty, Maggie Morse, Jeff Horing, Rob Epstein, M.D.

Investor POV

AI in financial services is here: How firms are adopting and where they’re stuck

Article

Thought Leadership

Market maps

Industry Insights

BioTech/Therapeutics

Finance & Accounting

Elan Arnowitz, Alessandro Luciano

Market maps

The state of the robotics ecosystem: The tech, use cases, and field deployment

Thought Leadership

Industry Insights

AI/ML Ops

Lonne Jaffe

Investor POV

Primed for reinvention: Video intelligence industry moves to the cloud

Blog

Article

Thought Leadership

Industry Insights

IT Mgmt

Arjun Mehta, Apoorva Goyal, Alex Debayo-Doherty

Investor POV

Financial services has a data problem: How AI is fueling innovation

Thought Leadership

Industry Insights

Finance & Accounting

Nicole Shimer, Elan Arnowitz

Investor POV

The next industrial revolution: How software is shaping the future of production

Thought Leadership

Industry Insights

Supply Chain & Logistics

Arjun Mehta

Investor POV

AI Agents are disrupting automation: Current approaches, market solutions and recommendations

Industry Insights

AI/ML Ops

Praveen Akkiraju, Sophie Beshar, Hunter Korn

Investor POV

Investors and CEOs need a climate risk strategy now more than ever. Here are 5 reasons why.

Industry Insights

Deven Parekh

Inside Insight

OUTsight

Celebrating Pride Month at Insight

Insight Partners

Article

Celebrating Women’s History Month at Insight

Insight Partners

Inside Insight

Celebrating Black History Month at Insight

Insight Partners

OUTsight

Celebrating Pride Month at Insight

Insight Partners

Article

Celebrating Women’s History Month at Insight

Insight Partners

Inside Insight

Celebrating Black History Month at Insight

Insight Partners

MORE INSIGHT NEWS